Ask ten banking executives to define modernization, and you’ll likely hear ten different answers. Some will point to cloud migration. Others will emphasize AI. A few will fall back on “digital transformation” – a term so overused that it has lost any precise meaning. This lack of clarity isn’t just semantic; it’s a root cause of why many modernization efforts stall or fail to deliver real impact.

At its core, retail banking modernization is not a technology initiative. It’s a deliberate shift in how the bank operates – replacing a model designed for the constraints, cost structures, and customer expectations of the 20th century with one built for today’s realities. That distinction is critical. When modernization is treated as a series of disconnected tech upgrades, banks often end up preserving the same inefficiencies and limitations.

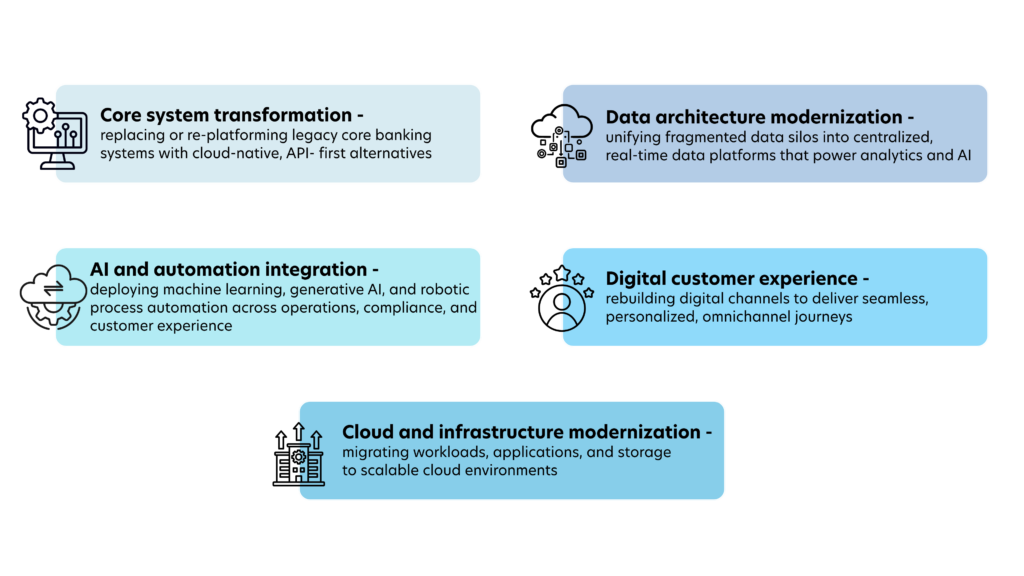

To understand what meaningful modernization actually involves, we need to view the five layers of modernization in banking that defines the scope as none of them can be addressed in isolation.

AI, for instance, is often positioned as the end goal, but its effectiveness depends entirely on the quality and accessibility of underlying data. That, in turn, is shaped by the bank’s data architecture – how information is structured, governed, and made available across the organization. But data architecture cannot be fixed in a vacuum; it is constrained by legacy core systems that were never designed for real-time, integrated data flows.

Similarly, efforts to scale digital products, whether mobile banking, lending platforms, or personalized services depend heavily on flexible, resilient cloud infrastructure. Without it, innovation remains slow, fragmented, and difficult to sustain. And even when all these foundational elements are in place, they only create value if they come together cohesively at the customer experience layer where functionality, usability, and trust ultimately determine success.

Modernization, then, is not about choosing between cloud, AI, or digital channels. It’s about aligning these layers into a coherent operating model – one where each investment reinforces the others, and where the whole is meaningfully greater than the sum of its parts.

These layers are not a checklist. They form a dependency chain. Leaders who understand that chain – and sequence their investment accordingly are the ones whose programs deliver lasting competitive advantage rather than isolated wins that stall.

For a deeper look at how leading banks are structuring this journey end-to-end, explore our perspective on retail banking transformation: https://www.quinnox.com/retail-bank-modernization/

Why ‘Digital Transformation’ Is Not Enough

Many banks conflate surface-level digital upgrades – launching a mobile app, moving email communications online – with genuine modernization. True modernization goes deeper: it means rebuilding the infrastructure that powers those experiences, so that innovation can happen continuously and at speed.

This is exactly why legacy modernization – not just digital layering – has become the foundation for sustainable transformation in banking. Learn how banks are making this shift successfully: https://www.quinnox.com/blogs/how-legacy-modernization-drives-digital-transformation-success-in-banks/

Business Case: Why Senior Leaders Are Prioritizing Modernization Now

The business case for retail banking modernization has never been stronger or more urgent. A convergence of competitive, financial, regulatory, and technological pressures is making the cost of inaction higher than the cost of transformation.

1. The Competitive Pressure: Fintechs Are Not Waiting

Digital-native challengers – neobanks were built on modern infrastructure from day one. They have no legacy debt, no mainframe dependency, and no 18-month product development cycles. Traditional banks using legacy technology take 12 to 24 months to launch new products; fintechs launch equivalent capabilities in 3 to 6 months. That is not a marginal difference. It is an existential gap.

The market share consequences are already arriving. According to Finacle research, non-incumbent challengers are projected to claim over 30% of the global retail banking market share by 2030. For established institutions that fail to modernize, BCG warns that their global cost-to-income ratio could rise to approximately 74% by 2030 compared to 63% in 2023 as maintenance costs compound and innovation capacity atrophies.

Legacy Cost Trap

Banks spend 70–78% of their IT budgets maintaining legacy systems – leaving only ~19% for innovation and new capability development. (The Fintech Times)

2. The Financial Case: Legacy Costs Are Spiraling

Most banking leaders significantly underestimate the true cost of their legacy estate. A comprehensive analysis by Deloitte found that banks underestimate the true total cost of ownership of legacy systems by 70 to 80%, with actual IT costs running 3.4 times higher than initially budgeted when all factors are accounted for, including compliance overhead, integration workarounds, incident response, and the opportunity cost of delayed innovation.

The numbers compound over time. IBS Intelligence Research says, global banks spent $36.7 billion maintaining outdated payment systems in 2022 alone – a figure projected to reach $57 billion by 2028. By the same year, banks that fail to modernize could lose over $57 billion in missed revenue, with 42% of that loss concentrated in payments alone.

Contrast this with the returns from modernization: institutions completing core modernization consistently report 30 to 40% reductions in IT maintenance costs, 25 to 35% reductions in infrastructure costs, and 15 to 20% overall operational cost savings – alongside a 40 to 60% acceleration in release cycles.

3. The Regulatory and Talent Case

Regulatory pressure adds another dimension to the business case. European and UK banks face compounding compliance obligations from PSD2, GDPR, ISO 20022 (mandatory from November 2025), and evolving AI governance frameworks, including the EU AI Act. Legacy systems spend 4.7 times more on compliance than modern equivalents, according to a Financial Conduct Authority study. That is not a sustainable cost structure.

The talent dimension is equally acute. Nearly one-third of COBOL programmers – the specialists who maintain core banking systems written in the 1960s and 70s – will retire by 2030. Younger engineers do not train in COBOL or JCL. The institutional knowledge locked inside legacy systems is aging out of the workforce, creating a talent crisis that makes modernization not a choice but an inevitability.

The Opportunity Cost Is the Hardest Cost to See

When a bank’s IT team spends 70%+ of their budget on maintenance, they are not building personalized lending tools, real-time fraud prevention, or AI-powered advisory services. The opportunity cost of legacy dependency – measured in products never launched, customers never retained, and revenue never earned – often dwarfs the direct cost of keeping old systems running.

The Legacy Problem: What's Actually Holding Retail Banks Back

Understanding what legacy systems are and what they cost – is essential before any modernization strategy can be credibly built. The term ‘legacy system’ is often used loosely.

In banking, it has a specific meaning: core platforms built primarily in the 1970s and 1980s, running on COBOL, batch-processing architectures designed for a world before real-time data, mobile devices, or APIs. Many of these systems have never been replaced because they work — they process trillions of dollars in transactions daily with exceptional reliability. That reliability is precisely what makes them so difficult to remove.

But reliability for yesterday’s banking model is not the same as fitness for today’s. The specific ways legacy systems obstruct modernization are well-documented:

| Legacy Constraint | Business Impact |

|---|---|

| Batch-processing architecture | Cannot support real-time payments, instant account opening, or live fraud scoring |

| No API compatibility | Cannot integrate with open banking ecosystems, fintech partners, or cloud services |

| Monolithic codebase | Minor updates require months of development, extensive QA cycles, and high consulting costs |

| COBOL dependency | Shrinking talent pool; knowledge risks retiring with the engineers who built the system |

| Fragmented data silos | Cannot build a unified customer view; AI and personalization remain aspirational |

| Security patching complexity | Patching windows are narrow; legacy systems experience 300% more cyberattacks |

The scale of the problem becomes visible in operational data: a UK parliamentary review documented that nine major UK banks and building societies – including Barclays, HSBC, and Lloyds – suffered 158 distinct IT failures between January 2023 and February 2025. These incidents, averaging over six per month, resulted in over 800 hours – or approximately 33 days – of cumulative downtime for customers.

Despite this, only a quarter of institutions have made back-office and core system modernization a top priority – with the majority still focusing investment on the front-end digital layer that sits atop the fragile infrastructure beneath.

The $57 Billion Cost of Doing Nothing

By 2028, banks that fail to modernize could lose over $57 billion – 42% of that in missed payments revenue alone. Legacy systems also experience 300% more cyberattacks than modern alternatives.

Core Banking Modernization: Strategies, and How to Choose

There is no single correct path to core banking modernization. The right approach depends on an institution’s risk tolerance, existing architecture complexity, contract timelines, and strategic ambition. What is consistent across successful transformations is that strategy precedes execution – and that the approach is matched to the organization’s actual capabilities, not the most aggressive possible timeline.

Four primary modernization strategies that dominate the industry today:

Strategy 1: The Strangler Fig (Phased Wrap-and-Replace)

The strangler fig approach is the most widely adopted strategy for mid-to-large institutions. It involves gradually routing new functionality through modern microservices and APIs while the legacy core continues to operate beneath. Over time, functionality is incrementally migrated away from legacy components until the original system can be decommissioned – ‘strangled’ by the modern system that has grown around it.

Citi’s transformation is the most instructive large-scale example. Operating in nearly 180 countries, Citi launched its modernization program in 2021 and had retired over 1,250 legacy applications by 2024 – without major service disruption. The key was sequencing: starting with lower-risk, non-customer-facing systems before migrating higher-stakes core functions. In parallel, Citi migrated critical applications to Google Cloud, building the infrastructure layer that will support AI and real-time analytics going forward.

This approach is best suited for banks with complex, multi-line-of-business architectures and where a full replacement would represent unacceptable operational risk.

Strategy 2: The Greenfield (Parallel Build)

The greenfield approach involves building an entirely new core banking platform alongside the existing one, then migrating customers and functions in coordinated waves. This delivers a cleaner architecture with less technical compromise, and a shorter overall timeline – but it requires higher upfront investment and significant change management capability.

This strategy is increasingly chosen by digital-focused banks or institutions, making major strategic pivots. Monument Bank in the UK is a contemporary example: built from scratch on a modern, cloud-native core with Everforth Quinnox as a key technology partner, Monument deployed Qyrus, AI-powered test automation platform, powered by Everforth Quinnox to validate complex cross-product customer journeys – including client onboarding, account opening, lending origination, and transactions – with a speed and coverage impossible with manual QA. The result was an AI-powered quality assurance partnership recognized with the TESTA 2025 award for automated testing excellence.

Strategy 3: Replatforming

Replatforming involves migrating existing applications to a modern runtime environment – typically cloud – while preserving core business logic and data structures. It is the fastest and lowest-risk path to gaining cloud infrastructure benefits without a full application rewrite. The tradeoff is that technical debt and architectural limitations largely persist: you gain infrastructure agility without fundamentally redesigning the system.

Replatforming is most appropriate as a first phase – capturing quick wins in infrastructure cost and reliability while longer-term transformation is planned.

Strategy 4: API-Led Modernization

API modernization decouples the core from the front-end and third-party integrations by wrapping legacy systems in modern APIs. This approach is particularly valuable where a full core replacement is not immediately feasible, but where digital experience, open banking compliance, and fintech partnerships cannot wait.

The case for API modernization is compelling: 61% of banks are actively investing in open banking technology, and the Open Banking ecosystem is projected to generate over $400 billion in revenue opportunities by 2027. Banks that cannot expose their services through modern APIs are locked out of this ecosystem entirely.

How to Choose Your Strategy

There is no universally correct path. The strangler fig works best for complex, multi-market institutions prioritizing risk control. Greenfield delivers the cleanest outcome for banks willing to make a larger upfront bet. Replatforming captures infrastructure gains quickly. API-led modernization unlocks ecosystem value without full core replacement. Most institutions ultimately pursue a hybrid – beginning with APIs and replatforming to unlock near-term capability, while executing a phased core replacement over a longer horizon.

AI & Automation as the Modernization Accelerator

If legacy system modernization is the foundation, AI and automation are the force multiplier. As of early 2025, 92% of global banks report active AI deployment in at least one core banking function – but adoption rates and depth of implementation vary enormously. The banks that are capturing the most value are those treating AI not as a standalone technology initiative, but as an accelerant that amplifies every other modernization investment.

AI in retail banking is reshaping three critical domains: operational efficiency, customer experience, and risk management.

Operational Efficiency: Automating the Work Behind the Work

JPMorgan Chase’s COIN (Contract Intelligence) platform is the most cited example of AI-driven operational transformation in banking. The platform reviews complex commercial loan agreements – documents that previously required legal teams to process manually – in seconds, saving an estimated 360,000 lawyer hours annually. This is not incremental efficiency; it is a category-level shift in how legal and compliance operations function.

JPMorgan then extended its AI ambition further: its LLM Suite – a proprietary generative AI platform — was deployed to 50,000 employees (15% of its global workforce) as of 2024, making it one of the largest enterprise LLM rollouts in financial services history. The bank estimates its AI initiatives are already delivering $1 to $1.5 billion in annual business value, with CEO Jamie Dimon publicly committed to embedding AI into every single one of the bank’s processes.

The bank’s total technology investment reached $17 billion in 2024 – the highest ever recorded from a financial institution – with approximately half allocated to innovation including AI and cloud infrastructure.

AI Interaction Scale

Wells Fargo’s Fargo virtual assistant – powered by Google AI – logged 242.4 million customer interactions in 2024, handling bill payments, balance inquiries, and account servicing through natural language.

Wells Fargo Annual Report, 2024

Customer Experience: From Transactions to Relationships

AI-powered chatbots and virtual assistants now handle 70 to 85% of inbound customer queries at retail banks in North America, with resolution accuracy rates reaching 91% in 2025. But the most sophisticated institutions are moving beyond reactive automation to proactive, personalized engagement.

For Instance, NatWest Bank demonstrates what AI-driven personalization at scale looks like in practice: since deploying machine learning across its fraud and engagement systems, NatWest achieved a 90% reduction in new account fraud while AI-powered personalization drove a fivefold increase in clicks on product offers – a direct revenue impact from more relevant, more timely customer communication.

Risk Management: Proactive Intelligence Instead of Reactive Response

DBS Bank’s AI early warning system monitors customer financial behavior in real time, identifying signs of distress before delinquency occurs. The system enabled DBS to take proactive, supportive action for more than 80% of identified at-risk customers – a performance that is categorically impossible through traditional manual processes.

On the fraud side, AI models trained on behavioral biometrics and transaction patterns are now the primary defense layer for leading banks. Real-time fraud scoring – enabled only by modern, cloud-native infrastructure – allows decisions to be made in milliseconds, at the point of transaction, rather than through post-hoc batch analysis.

For banking leaders, the critical constraint on AI value delivery is not the AI itself – it is the underlying data infrastructure. AI models are only as good as the data they are trained on, and fragmented, siloed, inconsistent data is the reason many AI pilots fail to scale. This is why data architecture modernization is not a downstream consequence of AI adoption – it is a prerequisite for it.

Dive deeper into our BFSI capabilities: https://www.quinnox.com/industry-banking-financial-services/

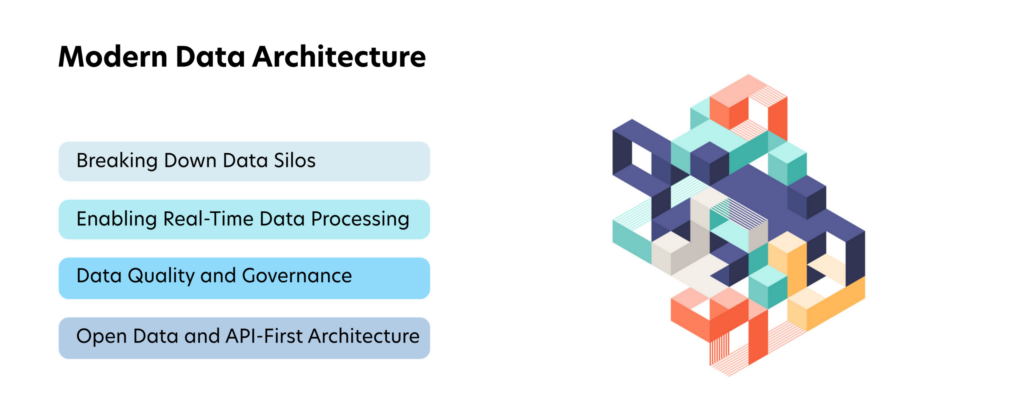

Building a Modern Data Architecture for Banking

Data is the foundational asset of the modern bank. Every AI use case, every personalized product recommendation, every real-time risk decision, every regulatory report – all of it runs on data. Yet for most traditional banks, data architecture remains the least visible and most underinvested dimension of their modernization agenda.

Fragmented data silos, inconsistent data quality, and the absence of a unified customer data layer are the reasons AI pilots fail to scale and personalization remains aspirational rather than operational.

Building a modern data architecture for banking means solving four interconnected problems:

1. Breaking Down Data Silos

Legacy banking architectures were built as a collection of purpose-specific systems: one system for deposits, another for loans, another for cards, another for compliance. Each generated its own data, in its own format, stored in its own location. The result is a fragmented landscape where no single system and no individual has a complete view of the customer or the institution.

Modern data architecture solves this by introducing a unified data layer – typically a cloud-based data lake or data Lakehouse that ingests, normalizes, and makes available data from all systems in real time. This unified layer is what enables a relationship manager to see a customer’s full financial picture in a single screen, or what allows an AI model to score creditworthiness on the basis of behavioral data rather than static application fields.

2. Enabling Real-Time Data Processing

Batch processing – where data is gathered, processed, and analyzed overnight – was the architecture of legacy banking. Real-time banking requires real-time data infrastructure: streaming pipelines that ingest transaction events, behavioral signals, and external data in milliseconds, and make them available immediately for fraud scoring, personalization, and customer service.

DBS Bank’s cloud migration – which drove a 30% improvement in operational efficiency and enabled over $500 million in annual AI-driven financial value – was fundamentally about building the real-time data infrastructure that makes AI analytics at scale possible. The cloud is not just cheaper storage; it is the infrastructure that makes real-time data processing economically viable.

3. Data Quality and Governance

Modern data architecture without rigorous data governance is a faster way to make bad decisions. Banks operating under GDPR, PSD2, and evolving AI transparency requirements cannot treat data governance as an afterthought. Data lineage, access controls, quality assurance, and explainability standards must be built into the architecture from the ground up – not added as a compliance overlay after the fact.

Everforth Quinnox’s data management and analytics practice addresses this directly: working with banking and financial services clients to securely migrate, reconcile, and integrate data across operations – with a focus on handling multiple formats, ensuring data integrity, and enabling insightful decision-making through robust, production-grade data pipelines.

Check out this essential read: Data Migration Checklist 2026: Your Essential Guide to a Successful Transition

4. Open Data and API-First Architecture

The third dimension of modern data architecture is openness. Open banking regulations require banks to make customer data available to authorized third parties through secure APIs. But beyond compliance, an API-first data architecture enables banks to build ecosystems: integrating fintech partners, embedding banking services in non-bank platforms (embedded finance), and creating new revenue streams through data-driven partnerships.

The revenue opportunity from this openness is substantial: Open Banking is projected to generate over $400 billion in revenue opportunities by 2027, with institutions that have built API-first data architectures positioned to capture a disproportionate share.

The Modernization Window Is Open - But Not Forever

The retail banking industry is in the middle of its most significant structural transformation in a generation. The pressures are real, the stakes are high, and the cost of delayed action is rising every quarter. But so too is the evidence that modernization – done with discipline and the right partners—delivers transformative outcomes.

For banking leaders, the mandate is clear: fix the legacy foundation, build real-time data infrastructure, deploy AI where it drives tangible business value, and reimagine the customer experience as a continuous, omnichannel relationship – not a series of disconnected transactions.

The institutions that will lead in 2030 are already executing against this agenda today—methodically, pragmatically, and with a clear focus on outcomes over optics. What’s increasingly separating leaders from laggards is not intent, but execution – how well this transformation is sequenced, integrated, and sustained.

That’s where Everforth Quinnox comes in. We partner with retail banks at every stage of their modernization journey – from legacy system assessment and core re-platforming to AI integration, real-time data architecture, and quality assurance at scale. Whether you’re defining a multi-year roadmap or unblocking a critical program, our focus is simple: move you from strategy to measurable outcomes, faster and with less risk.

If you’re looking to modernize with confidence – sequenced right, built to last, and without disrupting the operations your customers depend on – let’s start with what your program actually needs next.

Lead, Marketing, Everforth Quinnox

FAQ’s Related to Retail Banking Modernization

The four primary approaches are strangler fig (phased replacement), greenfield (build new core alongside old), replatforming (move to cloud without redesign), and API-led modernization (wrap legacy with APIs). Most banks adopt a hybrid model based on risk, cost, and speed.

AI is used to automate operations, enhance customer experience through personalization and chatbots, and strengthen risk management with real-time fraud detection and predictive analytics.

The biggest challenges include legacy system complexity, data silos, high transformation costs, regulatory compliance, and talent shortages—especially for maintaining outdated technologies.

Digital transformation focuses on improving front-end experiences, while retail banking modernization involves rebuilding the underlying core systems, data architecture, and infrastructure that enable long-term innovation.