Today we’re going to explore exactly how banks and insurers are turning generative AI into a measurable P&L impact. (And why 95% of them fail to.)

Here’s the thing:

Generative AI could add up to $340 billion a year to banking and up to $70 billion to insurance.

But, roughly 95% of enterprise GenAI pilots never deliver a single dollar of measurable P&L impact.

That’s not a technology gap. It’s an execution gap.

In this guide, we’ll show you:

- What generative AI consulting actually delivers for BFSI (hint: it’s not the model)

- The 6-step roadmap that separates the winners from the 95%

- The exact use cases producing real returns in banking and insurance right now

- How to get past the EU AI Act and US regulators without stalling your roadmap

- A 6-point checklist for choosing a consulting partner

Let’s dive right in.

Free Download: How to Build an AI Proof of Concept (PoC): A Strategic Roadmap

95% of GenAI pilots never make it to production. Yours doesn’t have to be one of them. This is the exact framework our teams use to take BFSI clients from idea to working prototype in days, not months.

What Generative AI Consulting Actually Delivers for Financial Services and Insurance

Generative AI consulting helps banks and insurers identify high-value GenAI use cases, design compliance-ready architectures, and scale deployments into production.

Sounds like every consulting pitch you’ve ever heard, right?

Here’s what makes it different from traditional data science consulting: it centers on foundation models, retrieval-augmented generation (RAG), and agentic workflows. Not building bespoke models from scratch.

And in regulated finance, that difference is everything.

Why does the consulting matter more than the model?

Here’s what the data actually shows:

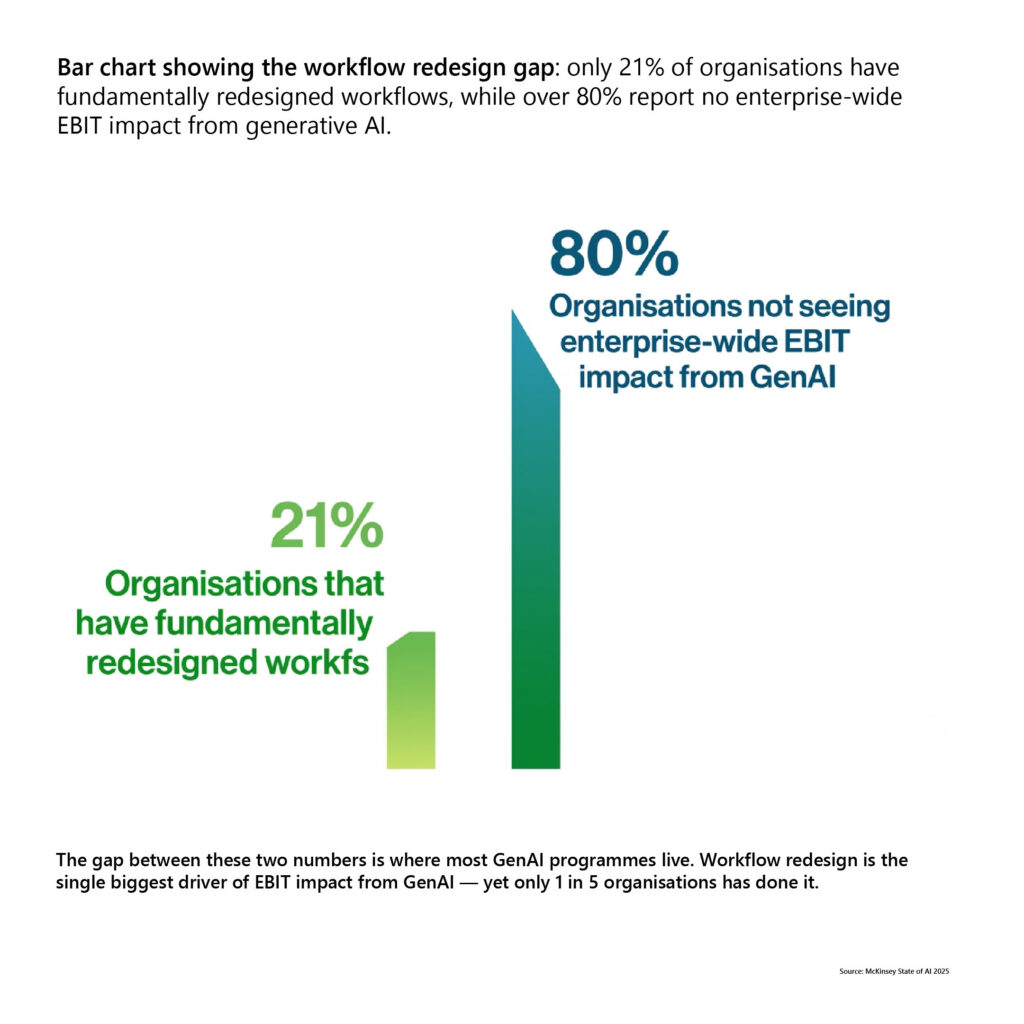

McKinsey’s State of AI research tested 25 factors to find what actually drives bottom-line impact from GenAI. Surprisingly, the answer wasn’t the model or the data stack. It was workflow redesign, which is by far the single biggest differentiator between firms that see EBIT impact and firms that don’t.

Here’s the uncomfortable part: only 21% of organizations have fundamentally redesigned their workflows.

The model isn’t the problem. It is the workflows, the people, and the change management around them where GenAI wins or dies.

That’s also why MIT’s GenAI Divide research found that companies purchasing AI from specialized vendors and building external partnerships succeed 67% of the time, compared to roughly one-third for firms building everything internally.

An experienced AI advisory services partner brings the workflow redesign, change management, and governance expertise that the 79% are missing.

The partner isn’t selling you a model. They’re selling you everything the model can’t do on its own.

For BFSI specifically, GenAI consulting covers five things generic consulting doesn’t:

1. Regulatory-aligned use case identification: Not the flashiest use cases. The ones that survive compliance review.

2. Compliance-first architecture: Governance designed in from day one. Not bolted on before launch.

3. Model governance and auditability: Every output traceable. Every decision explainable to an examiner.

4. Sensitive data handling: LLMs on customer financial data, without leaking a single record.

5. Sector-specific ROI measurement: Model outputs connected to combined ratio, cost-to-serve, and cycle time.

Think about the stakes for a second.

A retailer using GenAI for product descriptions risks a few awkward sentences.

A bank using GenAI in credit decisioning risks regulatory penalties, biased outcomes, and customer harm.

Same technology. Completely different risk math.

The GenAI Consulting Roadmap for Financial Services: Step-by-Step

Now let’s get tactical.

Here’s the 6-step sequence that separates the firms that scale from the 95% that don’t.

Skip a step and you’ll feel it later. (Usually in compliance review.)

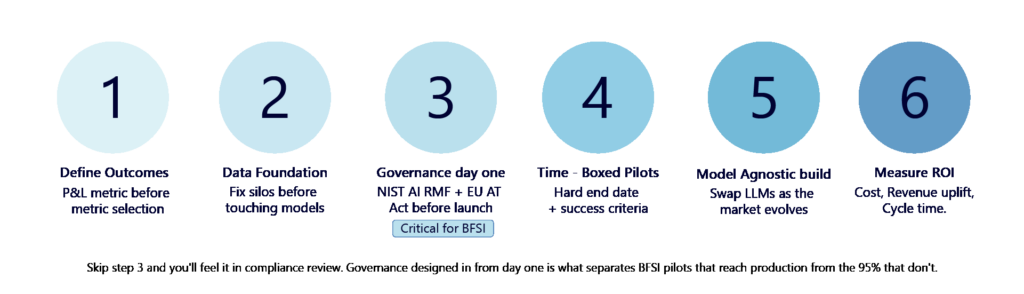

Step 1: Define Business Outcomes First

Start with the problem. Not the technology.

Every initiative gets tied to a P&L metric before a single model is selected.

“Reduce claims cycle time by 40%” is a project.

“Explore GenAI” is a budget leak.

Step 2: Establish the Data Foundation

GenAI built on fragmented, low-quality data produces confident nonsense.

Fix the silos first. And if your real data is too sensitive to use in model training, which in BFSI it usually is, synthetic data gives you a privacy-safe alternative that mirrors real-world patterns without exposing customer information. It’s how regulated firms train models without touching live PII.

Identifying those silos starts with knowing where they are. Our AI readiness assessment surfaces exactly that, before they become production incidents. The iAM Maturity Assessment gives you the scorecard to prioritize against.

Step 3: Implement Governance on Day One

Map your controls to the National Institute of Standards and Technology AI Risk Management Framework (NIST AI RMF) and the European Union Artificial Intelligence Act (EU AI Act) before deployment. Not after.

(We’ll show you exactly what that means for BFSI in the compliance section below.)

Step 4: Execute Time-Boxed Pilots

Run focused experiments with predefined success criteria and a hard end date.

No success criteria = impressive demos and zero defensible evidence.

Building that defensible evidence starts with a structured PoC. Our AI proof of concept guide covers the full methodology, while the AI PoC strategic roadmap is the condensed version, if your team wants to act on immediately.

One more thing on pilots: if your PoC needs data but your production data is off-limits, synthetic data generation lets you simulate realistic BFSI scenarios – fraud patterns, claims volumes, transaction histories – without compliance exposure. It’s built into QAI Studio for exactly this reason.

Step 5: Deploy Layered, Model-Agnostic Architecture

The LLM market changes quarterly.

Build systems that let you swap models without rebuilding the stack.

Firms that locked into a single model vendor in 2024 learned this lesson the expensive way.

Step 6: Measure ROI Relentlessly

Cost reduction. Revenue uplift. Cycle-time compression.

But here’s what most firms miss: you can’t measure impact if you didn’t measure the starting point.

Before you deploy a single model, capture your baselines. How long does a claims adjuster take to process a submission today? What’s your current false positive rate in fraud detection? How many pages does an underwriter review per day? These numbers, your pre-AI benchmarks, are what give your post-deployment results meaning.

A bank that reduces AML review time from 4 hours to 40 minutes has a story. A bank that says ‘our GenAI improved AML efficiency’ has a slide.

Capture the before. Measure the after. Show the delta. That’s what survives a board review.

If you can’t show the number, the programme dies at the next budget review.

Simple as that.

Generative AI Use Cases in Banking and Financial Services

So where is the money actually coming from?

The banking use cases delivering real returns today share one trait: they target document-heavy, language-heavy workflows that classical automation never cracked.

Here are the big five:

Customer experience transformation through conversational AI. The difference between a 2020 chatbot and a 2026 GenAI assistant isn’t the interface – it’s grounding.

Modern assistants use RAG to pull real-time account data, transaction history, and product context. So “why was I charged this fee” gets a specific, accurate, personalized answer in one interaction instead of a hold queue and a transferred call. First contact resolution rates go up. Escalations go down. And customers stop calling at all for routine queries.

Compliance and AML automation: Regulatory updates arrive as 1,000-plus page documents. GenAI summarizes them in minutes, flags the sections relevant to your products, and drafts suspicious activity reports that analysts review instead of write.

Credit decisioning augmentation: GenAI doesn’t replace credit models. It explains them. Plain-language narratives alongside model scores give regulators the transparency they demand.

Document intelligence at scale: Loan applications. Trade confirmations. Broker submissions. Multimodal models extract structured data from all of them, with audit trails.

Advisor productivity: Pre-meeting briefs, portfolio summaries, and personalized recommendations generated in seconds. Advisors spend their hours advising instead of assembling.

KYC onboarding and due diligence. Identity verification, sanctions screening, source of funds, beneficial ownership – KYC is a compliance analyst’s most document-heavy day. GenAI extracts, cross-references, and summarizes it all in minutes, with a full audit trail attached. What used to take two days now takes two hours.”

The same agent logic that cuts through banking’s document backlog applies even more forcefully in insurance, where a single underwriting submission can run to 200 pages and turnaround time is a direct competitive differentiator.

Picture this:

An underwriter opens a 200-page commercial submission at 9:00 AM.

By 9:02, an AI agent has already extracted the risk data, checked it against appetite guidelines, flagged two exclusions, and routed the file with a summary attached.

That’s the delay reduction in practice.

Agents triage incoming submissions, pull structured data out of unstructured documents, flag ineligible risks instantly, and route only the complex cases to humans.

The humans handle judgment. The agents handle volume.

The result: Submission-to-quote times drop from days to hours. And underwriters review 3x the cases without reviewing 3x the paper.

Generative AI Use Cases in Insurance

Insurance is the most document-intensive industry in financial services.

This makes it the industry where generative AI changes the most.

Quick note on framing: Classical AI has scored risks and detected fraud for a decade. What follows is what LLMs added. The delta. Not the whole history.

Underwriting triage: LLMs read the entire 200-plus page submission instantly. They extract the schedule of values, compare against portfolio benchmarks, and flag ineligible risks before a human opens the file. Pre-GenAI automation could route documents. It couldn’t read them.

Claims automation: Multimodal models process damage photos and medical records together, generate settlement recommendations, and settle routine claims in minutes through straight-through processing. The adjuster’s queue contains only claims that genuinely need an adjuster.

Free Download: How to Build an AI Proof of Concept (PoC): A Strategic Roadmap

95% of GenAI pilots never make it to production. Yours doesn’t have to be one of them. This is the exact framework our teams use to take BFSI clients from idea to working prototype in days, not months.

Get the Guide →

Policy document generation: Policy wordings. Endorsements. Renewal communications personalized to each policyholder’s history. These are generation tasks. And generation is precisely what pre-GenAI automation couldn’t do.

Customer service and distribution: GenAI assistants give agents real-time coverage comparisons and quote generation during live customer conversations. Not after them.

Actuarial support: GenAI compresses the data gathering and cleaning that eats most of an actuary’s day. More analysis. Less janitorial data work.

Compliance in GenAI isn’t a gate you pass through at the end. It’s the architecture you build from the beginning. Every Insurance firm we work with that got this right treated governance as a design principle, not a checklist.

Krishna Kumar Chakkirala

Vice President of AI & Data, Everforth Quinnox

That’s just one of dozens of ways AI is reshaping insurance operations. Our 25+ AI use cases in insurance covers the full landscape across underwriting, claims, distribution, and servicing.

AI Compliance and Governance for Generative AI in Financial Services

Here’s where most BFSI GenAI programs stall.

Not at the technology, but at the compliance review.

The good news? The rules are knowable. You just have to design for them from the start, not scramble to retrofit them at go-live

Let’s go through what actually applies to you

The EU AI Act treats your core use cases as high-risk.

Both credit scoring and insurance underwriting are explicitly named in Annex III of the Act.

That means mandatory documentation, transparency obligations, human oversight, and conformity assessment before you go live. Enforcement deadlines run through 2026 to 2028 – so the clock is already ticking.

And if you’re wondering whether the penalties are serious: up to €35 million or 7% of global annual turnover, whichever is higher.

Put that number in your next board deck.

The NIST AI RMF is becoming the de facto US standard.

- You’ve probably already seen it in vendor questionnaires. Its four functions – Govern, Map, Measure, Manage – are increasingly what examiners expect your model risk programme to reflect. If you haven’t mapped to it yet, start now.

- And then there’s the US sector-specific layer on top of all that:

- The NAIC Model Bulletin and the AI Systems Evaluation Tool now guide state insurance examiners

- The Colorado AI Act adds state-level obligations

- SEC and FINRA guidance covers AI in securities

- The Basel Committee has published principles for AI and ML in banking

None of these wait for the EU timeline.

Data sovereignty deserves its own conversation.

If your data can’t leave the building – and in most regulated BFSI environments, it can’t – you need on-premises, private cloud, or air-gapped deployment from day one. Not retrofitted in phase three. Decided upfront. Retrofitting sovereignty into a SaaS-first architecture is painful and expensive.

Hallucination isn’t just a quirk. It’s a liability.

An LLM that fabricates a regulatory citation or invents a transaction history creates real legal exposure. Retrieval grounding, output validation, and guardrails aren’t optional extras.

Do NOT deploy customer-facing GenAI without output validation.

One more thing: your employees are already using AI tools you haven’t approved.

That’s Shadow AI, and it’s happening in every financial institution right now. The smart response isn’t a ban. It’s converting that grassroots demand into sanctioned, governed enterprise systems before sensitive data walks out the door.

At the bottom of all of it sits the same requirement: human-in-the-loop design and explainability. Regulators don’t accept “the model decided.” Someone on your team has to be able to explain every high-stakes output. Build for that from the start.

Building for it from the start is exactly what our AI-Powered Compliance capability is designed for. Our guides on data governance for AI and AI compliance best practices cover the foundations.

Agentic AI Consulting for Financial Services: What Comes After GenAI

Here’s the entire shift in one line:

GenAI reads and writes. Agentic AI reasons and acts.

Where generative models produce content for humans to act on, AI agents plan, execute, and iterate across multiple systems. On their own.

In BFSI, that unlocks workflows automation never touched:

- Autonomous fraud investigation. An agent detects the anomaly, pulls transaction history, checks watchlists, assembles the evidence file, and drafts the case summary. Your investigator reviews a finished package instead of building one.

- Continuous compliance monitoring. Agents scan regulatory feeds 24/7, flag changes relevant to your products, and map them to affected policies before your next compliance meeting. See how this works in practice in our guide to AI-powered regulatory change management.

- KYC/AML onboarding orchestration. One agent coordinates identity verification, sanctions screening, and document validation across multiple data sources. End to end.

- Exception handling beyond RPA. Robotic process automation breaks when inputs vary. Agents reason through the variance.

Now the question every banking risk officer asks:

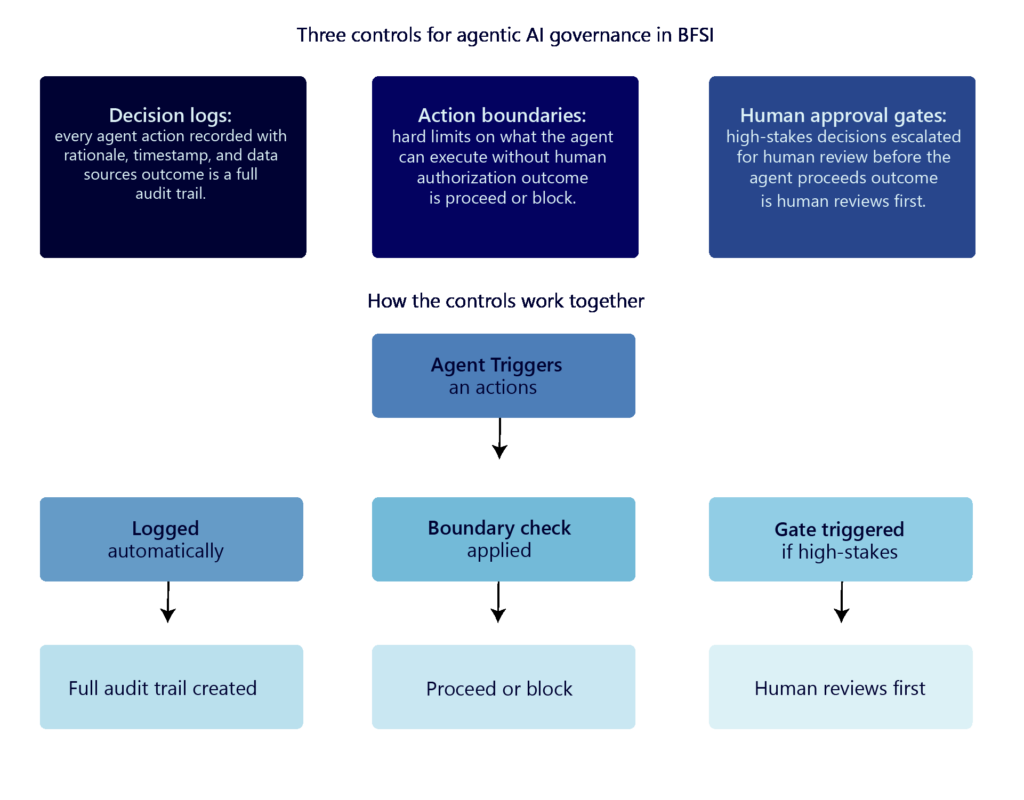

How do you audit an agent’s decisions?

Three controls:

1.Decision logs that record every action and its rationale

2. Action boundaries that hard-limit what an agent can do without approval

3.Human approval gates for anything high-stakes

Designing those autonomy levels is the core advisory deliverable. Because the right answer is different for a fraud agent (99.9% accuracy required, speed secondary) and a service agent (speed required, 90% resolution acceptable).

And once those autonomy levels are set and your agents go live, the work doesn’t stop. Our agent management services framework keeps agents governed, monitored, and performing after deployment.

What to Look for in a Generative AI Consulting Partner for Financial Services

Here’s the 6-point checklist we’d use if we were evaluating ourselves.

Steal it.

1. Productiontrack recordin regulated industries: Pilots are easy. Ask for outcomes from production BFSI deployments comparable to yours. If every reference story ends at “successful proof of concept,” keep looking.

2. Compliance-firstmethodology:Can they map controls to the EU AI Act and NIST AI RMF from day one? If governance shows up in phase three of their proposal, it’ll show up in phase three of your problems.

3. Data sovereignty capability:On-premises, private cloud, and air-gapped options, with certifications to prove data handling discipline. For regulated data, this isbinary. They can or they can’t.

4. Deep legacy integration experience:Core banking platforms. Policy administration systems. Claims engines. GenAI thatcan’t reach your systems of record is a demo, not a deployment. And demand total cost of ownership transparency, including integration.

5. Full lifecycle capability:Strategy through deployment through ML/LLM Ops. Strategy-only firms hand you a beautiful roadmap and leave you stranded at implementation.

6. Platform accelerators:Pre-built frameworks and accelerators like QAI Studio compress time-to-value from months to days. Building everything from scratch is how budgets die.

Two more data points worth knowing:

McKinsey’s research on GenAI operating models in banking consistently shows that centrally led programmes outperform fragmented, decentralized efforts. Your consulting partner should have a view on operating model, not just technology. If they don’t bring it up, ask.

The technology is only half the equation. The other half is getting your people, processes, and culture ready for what comes after deployment. Our guide to building an AI-ready workforce covers the change management frameworks, training approaches, and adoption strategies that separate BFSI firms that scale GenAI from those that stall.

And if you’re a mid-market bank or insurer, ask about a fractional engagement model. Think of it as hiring a senior AI strategist on retainer rather than as a full-time executive, where you get the expertise without the headcount cost. Most mid-market firms don’t know this option exists, and it’s often the fastest way to get a credible GenAI programme off the ground.

And if you’re still weighing up providers, our guide on how to choose an AI consulting firm gives you the full evaluation framework to compare across industries.

How Everforth Quinnox Helps Financial Services and Insurance Firms Adopt Generative AI

Everything in this guide reflects how we actually work with banks and insurers.

Advisory and Assessment. We start with an AI maturity assessment that factors your regulatory constraints in from the start, so you invest where compliance review won’t kill the project.

Proof of Concept. Rapid prototyping for BFSI use cases like claims automation, compliance reporting, and customer onboarding through our AI PoC development services. With Everforth Quinnox AI (QAI) Studio’s 50+ accelerators and 70+ mapped use cases, ideas become working prototypes in days. Not months.

Build and Integration. Production-ready GenAI integrated with your core banking systems and insurance platforms. Not bolted alongside them.

Governance and Security. Compliance-aligned frameworks covering the EU AI Act, NIST AI RMF, and sector-specific regulations — built in from day one.

ML/LLM Ops. Monitoring, retraining, drift detection, and token cost optimization so models stay accurate and affordable long after launch. Explore the full capability set on our AI & Data Services page.

Behind it all: 250+ AI and data experts who’ve done this in regulated environments before.

Ready to move from pilot purgatory to production? Connect with our AI experts.

The firms we see breaking out of pilot purgatory aren’t the ones with the biggest AI budgets. They’re the ones that picked one high-impact workflow, redesigned it around GenAI, and measured everything from day one. That’s where we start every engagement.

Krishna Kumar Chakkirala

Vice President of AI & Data, Everforth Quinnox

The Bottom Line: The S-Curve of Adoption

GenAI in financial services is moving through a predictable curve.

Phase one was horizontal productivity: emails, summaries, marketing copy.

The phase happening right now is core process transformation: automated underwriting, continuous compliance monitoring, agentic operations.

The firms that build the control plane – governance, architecture, measurement – capture the steep part of the S-curve. The rest stay in pilot purgatory.

The technology is ready. The regulations are knowable. The roadmap is six steps long, and you just read it.

The only question left: will you run it with a partner who’s done it in regulated finance before?

Assistant Manager, Marketing, Everforth Quinnox

FAQs Related to Generative AI Consulting

Start with three questions:

– Do they have production deployments in regulated industries, not just pilots?

– Can they map governance controls to the EU AI Act and NIST AI RMF from day one?

– Do they offer full lifecycle support, from strategy through ML/LLM Ops?

Add data sovereignty capability and legacy core system integration experience, and you’ve filtered out most of the market. Platform accelerators that compress time-to-value are the final differentiator.

Map every GenAI initiative to the applicable frameworks before deployment. Under the EU AI Act, credit scoring and insurance underwriting are high-risk AI systems requiring documentation, transparency, and human oversight, with penalties up to €35 million or 7% of global turnover. In the US, align model risk programs to the NIST AI RMF and track sector rules like the NAIC Model Bulletin. Then add output validation, audit trails, and human approval gates for high stakes decisions.

Four use cases are delivering measurable returns today: underwriting triage, where LLMs extract and assess data from 200-plus page submissions instantly; claims automation, where multimodal models process damage photos and medical records to settle routine claims in minutes; policy document generation, including personalized wordings, endorsements, and renewals; and GenAI-assisted customer service providing real-time coverage comparisons during live interactions.

AI agents triage submissions the moment they arrive: extracting risk data from unstructured documents, checking it against appetite guidelines, flagging ineligible risks instantly, and routing only complex cases to human underwriters with a summary attached. The result is submission-to-quote time dropping from days to hours, with underwriters reviewing significantly more cases while focusing exclusively on judgment calls.

Generative AI reads and writes: it summarizes regulations, drafts reports, and explains credit decisions, but a human acts on the output. Agentic AI reasons and acts: it executes multi-step workflows across systems autonomously, like investigating a fraud alert end to end or orchestrating KYC checks across multiple data sources. In banking, agentic AI requires stricter controls: decision logs, action boundaries, and human approval gates for high-stakes actions.