The insurance industry is entering a period of profound transformation driven by artificial intelligence (AI). For decades, insurers have relied on traditional actuarial models, manual workflows, and legacy IT systems to assess risk, price policies, and process claims. While these methods provided stability, they also created inefficiencies that limited operational agility and slowed customer service. Today, increasing data volumes, rising customer expectations, and intensifying competition are forcing insurers to rethink how they operate. Artificial intelligence is emerging as a key technology enabling this transition.

Advances in artificial intelligence, particularly machine learning (ML), natural language processing, and predictive analytics are enabling insurers to process information at a scale and speed that was previously impossible. These technologies are helping organizations move beyond static models toward dynamic, real-time insights that improve operational efficiency and customer experience.

Despite the significant opportunities that AI offers, integrating it into core insurance operations remains a complex undertaking for many organizations. Industry research shows that while 76% of insurers are experimenting with AI, only about 7% have successfully scaled AI solutions enterprise-wide, indicating a gap between experimentation and full operational deployment. Several factors contribute to this challenge, but one of the most prominent is the continued reliance on legacy infrastructure, which often restricts data integration, limits scalability, and complicates the deployment of advanced analytical systems.

As the industry moves toward a more intelligent and data-driven future, organizations that embrace AI strategically will be better positioned to deliver superior customer experiences, improve operational efficiency, and remain competitive in a rapidly evolving market.

Market & Industry Overview:

Artificial intelligence is quickly moving from experimentation to mainstream adoption across the insurance industry. What once began as limited pilots in analytics and automation is now being embedded across underwriting, claims processing, fraud detection, and customer engagement. As insurers face increasing pressure to improve operational efficiency and deliver faster, more personalized services; AI is becoming a central pillar of digital transformation across the insurance value chain.

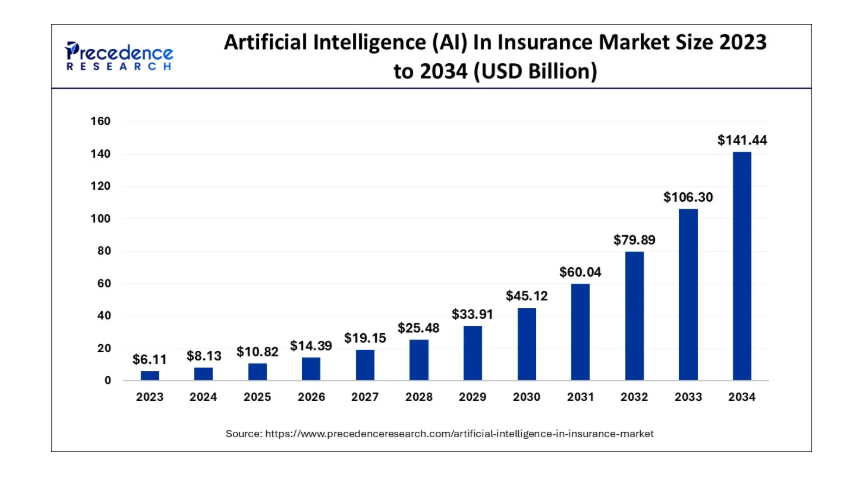

Precedence Research estimates that the global AI in insurance market size estimated at USD 10.82 billion in 2025 is expected to increase from USD 14.39 billion in 2026 to USD 176.58 billion by 2035, signaling a growth of 32.21% from 2026 to 2035.

This rapid expansion reflects the accelerating pace at which insurers are investing in AI-driven platforms to streamline operations, enhance risk modeling, and improve decision-making. Compared with earlier waves of technology adoption in the sector, the scale and speed of AI adoption signal a fundamental shift in how insurance organizations operate and compete.

For insurance leaders, this growth carries significant implications. AI is no longer simply a tool for incremental efficiency - it is becoming a strategic capability that shapes product innovation, operational agility, and customer experience.

Key Insurance Industry Challenges That AI Can Address

Artificial intelligence is gaining attention not only as a technological innovation but also as a practical solution to address several persistent challenges that have historically constrained efficiency, accuracy, and customer satisfaction.

Across areas such as claims processing, underwriting, fraud detection, risk assessment, and customer engagement, insurers face operational bottlenecks that can lead to delays, financial losses, and limited decision-making agility. The following sections highlight some of the most significant challenges within the insurance value chain and explain why these issues are becoming more difficult to manage using traditional approaches.

1. Inefficiencies in Claims Processing

Claims management is one of the most resource-intensive functions within an insurance organization, involving multiple stages such as document verification, damage assessment, policy validation, and payment authorization. These activities often rely heavily on manual review and coordination across different teams, making the process complex and time-consuming.

A significant challenge also arises from the nature of the information submitted with claims. Insurers must process a wide range of unstructured data, including photographs of damages, scanned documents, handwritten forms, invoices, and detailed incident descriptions. Manually reviewing, interpreting, and validating this information can slow down decision-making and introduce inconsistencies in the evaluation process.

Such delays impact the overall customer experience. When policyholders face prolonged waiting periods during what is often a stressful situation, it can affect their confidence in the insurer and influence long-term customer satisfaction and loyalty.

2. Limited Precision in Risk Assessment

Risk assessment lies at the core of insurance operations. Insurers must evaluate the likelihood of future losses in order to price policies accurately and maintain financial stability. Traditionally, this process has relied heavily on historical averages, demographic indicators, and relatively static risk models.

While these models have served the industry for many years, they often lack the ability to incorporate real-time or behavioral data. As a result, risk assessments may not fully reflect the dynamic nature of modern risk environments. Factors such as changing climate patterns, urbanization, evolving mobility behaviors, and emerging health risks introduce new complexities that traditional models may struggle to capture.

Another challenge involves the sheer volume and diversity of available data. Insurance companies now have access to information from telematics devices, connected homes, wearable technology, and environmental monitoring systems. Extracting meaningful insights from these datasets requires analytical capabilities beyond conventional statistical tools.

Without more advanced analytical methods, insurers may face difficulties in accurately identifying high-risk scenarios or adapting pricing strategies to reflect emerging trends.

3. Complexity and Delays in Underwriting

Underwriting is the process through which insurers evaluate whether to issue a policy and determine the terms under which coverage will be provided. This process often requires reviewing extensive documentation, analyzing multiple data points, and applying complex risk evaluation criteria.

One major challenge in underwriting is the time required to gather and validate information. Data relevant to underwriting decisions may come from multiple sources, including medical records, financial documents, credit histories, and external databases. Collecting and interpreting this information manually can significantly slow down the underwriting process.

Another difficulty lies in achieving consistency in underwriting decisions. Human judgment plays a significant role in evaluating risk, which can sometimes lead to variations in how policies are priced or approved. Here any inconsistency may result in mispriced policies, increased exposure to risk, or missed business opportunities.

4. Persistent Challenges in Fraud Detection

Insurance fraud represents a substantial financial burden for the industry worldwide. Fraudulent activities can take many forms, including exaggerated claims, staged accidents, identity manipulation, and organized fraud networks.

One of the most difficult aspects of fraud detection is identifying suspicious behavior early in the claims process. Fraudsters often exploit system loopholes or attempt to mimic legitimate claims, making detection difficult through traditional rule-based methods.

Another challenge is the scale at which insurers must operate. Large insurance providers process thousands of claims every day, making it impractical for human investigators to review each case thoroughly. As a result, fraudulent claims may sometimes go unnoticed, leading to financial losses.

Conversely, overly aggressive fraud detection measures may also create problems by incorrectly flagging legitimate claims for investigation, which can delay payments and negatively impact customer relationships. Hence, balancing fraud prevention with efficient claims processing remains a complex challenge for insurers.

5. Fragmented Data and Information Silos

Insurance companies generate vast amounts of data across multiple departments, including underwriting, claims management, customer service, and policy administration. However, this information is often stored across separate systems that do not easily communicate with one another.

These fragmented data environments create several operational limitations. Decision-makers may lack access to a complete view of policyholder history, making it harder to evaluate risk accurately or identify patterns of fraudulent behavior.

Data silos also slow down analytical processes, as teams must manually gather information from multiple sources before conducting analysis. This fragmentation limits the ability of insurers to derive meaningful insights from the data they already possess.

As insurance ecosystems continue to expand and incorporate new data sources, effective data integration becomes increasingly critical.

6. Increasing Operational Costs

Manual processes across underwriting, claims management, compliance, and customer service contribute significantly to operational costs in insurance organizations. Tasks such as document verification, policy administration, and regulatory reporting often require substantial human involvement.

As the volume of policies and claims increases, maintaining these manual workflows can become both inefficient and expensive. Operational teams may struggle to keep up with growing workloads, leading to longer processing times and higher administrative expenses.

Reducing operational complexity while maintaining service quality is therefore a key challenge for insurers seeking to remain competitive.

7. Evolving Customer Expectations

Customer expectations in the insurance industry have shifted significantly in recent years. Consumers increasingly expect the same level of digital convenience and responsiveness they experience in other industries such as banking, retail, and telecommunications.

Traditional insurance processes, which often involve lengthy forms, delayed responses, and complex documentation requirements, may not meet these expectations. Customers now prefer digital claim submissions, real-time updates, and faster resolution timelines.

Failure to deliver streamlined digital experiences can lead to dissatisfaction and increased customer churn, particularly as new digital-first insurers enter the market.

8. Difficulty in Proactive Risk Prevention

Historically, insurance has been largely reactive in nature. Policies are designed to compensate for losses after an event occurs rather than preventing those losses from happening in the first place.

However, with the growing availability of real-time data from connected devices and environmental monitoring systems, insurers now have opportunities to shift toward more proactive risk management models.

The challenge lies in effectively analyzing these continuous data streams and identifying meaningful signals that indicate emerging risks. Without advanced analytical tools, insurers may struggle to translate raw data into actionable insights that help prevent accidents, property damage, or health complications.

AI Use Cases in Insurance Distribution, Underwriting, Claims

From enabling personalized product recommendations in distribution, to improving risk evaluation and pricing in underwriting, and accelerating claims assessment and fraud detection, AI is becoming a critical enabler of efficiency, accuracy, and scalability. As insurers continue to modernize their operations, AI-powered solutions are redefining how policies are sold, risks are assessed, and claims are processed.

The following sections explore key AI use cases across insurance distribution, underwriting, and claims, highlighting how these technologies are helping insurers overcome long-standing operational challenges while delivering greater value to customers and stakeholders.

Distribution

- Advanced customer segmentation: AI and ML can mine digital and social data to build rich prospect segments, enabling more effective targeting and channel choice.

- Adaptive channel allocation: AI analyzes customer behavior and history to match each prospect with the most effective distribution channel (online, agent, etc.) and even optimize agent workload/schedules.

- Demand analysis & product configuration: AI processes historical sales and customer data to predict emerging demand trends by channel. For example, identifying a lapse in renewals among millennials and automatically targeting them with tailored LinkedIn campaigns or new products.

- Automated policy recommendations: NLP-driven systems ask customers questions and convert answers into machine-understandable inputs, extracting sentiment and risk appetite to auto-suggest the optimal policy (streamlining quote generation without an agent).

- Next-best action for agents: AI engines recommend precisely which sales action an agent should take next (e.g. best product to offer or which customer to call), effectively serving as a dynamic sales coach.

- AI-powered lead generation: AI analyzes data to identify high-potential leads and automatically route them to agents.

- Personalized sales support (agent productivity): AI generates personalized talking points and product bundles for agents. For example, AI engine provides agents with tailored script prompts and the optimal agent-product pairing, leading to higher cross-sell and churn reduction.

- Upselling and cross-selling optimization: AI matches customers with the right additional products and trained agents to maximize conversion.

- Personalized Premiums: Traditional premium models fail to account for individual driving behaviors, leading to less accurate pricing and missed opportunities for customer engagement. This is where AI steps in providing accurate and personalized insurance premiums based on real-time driving behavior and vehicle data using vehicle sensors.

Underwriting

- Automated application intake: AI-driven processing of submissions – extracting and validating data from new-business forms, loss runs, statements of value, etc. to speed up underwriting. This frees underwriters from manual data entry so they can focus on decision-making.

- Enhanced risk assessment: AI analyzes vast data (e.g. past claims, applicant data, medical histories) to score and mitigate risk. By automating evaluation of documentation, AI enables faster, more accurate risk decisions.

- Underwriting case management: AI tools automate workflow tasks (prioritizing cases, assigning to the right underwriter, tracking case status) to streamline the underwriting process. For example, AI can automatically route complex cases and improve collaboration between underwriting teams.

- AI-driven decision support (fraud and misrepresentation detection): AI models flag likely fraud or misrepresentation before policy binding.

- Automated underwriting alerts: AI continually scans bound policies and new submissions, generating alerts for any anomalies (e.g. inconsistent data, overvalued assets).

- Submission triage and document handling: AI automatically extracts information from incoming submissions and questionnaires, assigns a risk score, and triages them. It can also detect missing documents in broker submissions and automatically request them to close underwriting gaps.

- Supplemental questionnaire processing: AI parses unstructured supplemental forms (capturing industry-specific risk factors or details) and populates key underwriting fields, improving risk models and quote speed.

- Policyholder communication: AI-powered chatbots and portals automate routine policy inquiries and updates, allowing underwriters to spend more time on complex tasks. For example, intelligent interfaces handle status questions and auto-generate correspondence, improving the customer experience while underwriting.

Claims

- Automated FNOL and data intake: AI automates first-notice-of-loss (FNOL) processing by extracting data from forms, photos, and documents. Intelligent claims agent ingests any format (images, PDFs, handwritten notes), pulls key fields (date of loss, parties, damages, etc.), verifies policy details, and auto-routes the claim. This slashes manual intake time and accelerates claim setup.

- Data extraction and verification: AI systematically extracts and verifies all claim-related data (accident reports, estimates, invoices) with minimal human effort. AI/ML models can also map extracted fields to legacy systems for faster downstream processing.

- Automated damage assessment: AI-driven image analysis evaluates damage photos (vehicles, property, etc.) to support claim decisions. For instance, AI can compare uploaded vehicle images to past claims to estimate repair needs, enabling quicker and more accurate settlements. This replaces slow manual photo reviews with instant insights.

- Claims fraud detection: AI continually analyzes claims data and images to flag suspicious patterns. It can spot anomalies that humans miss (e.g. subtle injury patterns, inflated repair estimates, staged claims). Insurers can use AI agents to score claims by fraud risk and generate investigation leads with supporting evidence.

- Claims triage and routing: AI agents automatically assess incoming claims for severity and complexity, then prioritize and route them. For example, a “Claims Triage Agent” classifies new claims by seriousness and fraud likelihood, ensuring high-risk cases get fast attention.

- Coverage compliance (COI analysis): AI checks that a claim is covered by the policy. Specifically, an AI “Coverage Analysis Agent” ingests the claim-related Certificate of Insurance and contract requirements, extracts coverage details and limits, compares them to what the loss requires, and flags any deficiencies. This ensures, for example, that a subcontractor’s lapse in coverage is caught and handled properly.

Predictive Modelling

- AI predicts health outcomes for policyholders by analyzing medical history, lifestyle factors, and genetic data. Traditional methods lack the predictive capability to foresee future health issues, leading to suboptimal coverage and higher claim costs. Improved coverage accuracy, reduced claim costs, and enhanced health management by predicting potential health risks.

- Organizations struggle to identify high-risk areas and predict potential claims using traditional methods, leading to preventable losses. This is where AI models help predict potential claims for risk mitigation by analyzing historical data, weather patterns, and customer behaviors to minimize future claims and financial losses.

Don’t see your use case above? Explore our full collection of 50+ real-world AI applications in insurance and discover how AI can drive impact for your business.

How Everforth Quinnox Helps Insurers Operationalize AI at Scale

For many insurers, the challenge with AI is not recognizing its value but operationalizing it across the enterprise. Initiatives often remain limited to pilot programs due to integration complexity, fragmented data environments, and the effort required to build and maintain AI systems internally. To overcome these barriers, organizations need an approach that delivers AI capabilities in a way that is scalable, adaptable, and aligned with real business processes.

Quinnox addresses this need through two key capabilities designed to accelerate enterprise AI adoption:

QAI Studio – AI Development and Orchestration Platform

Quinnox’s AI innovation hub, Quinnox AI (QAI) Studio, provides the foundation for building, training, and deploying AI solutions tailored to insurance use cases. QAI Studio enables teams to work with diverse data sources, design intelligent workflows, and operationalize AI in a controlled and scalable environment.

By bringing together data engineering, model development, and automation within a unified ecosystem, QAI Studio helps organizations move from ideas to POCs and to production in just days rather than months. The platform is supported by 50+ AI accelerators, 250+ data experts, 50+ AI agents, and 70+ industry use cases, enabling faster development of AI-powered solutions across core insurance operations.

QAI Studio also offers a structured pathway to develop and validate AI proof-of-concepts (PoCs) that can quickly evolve into production-ready solutions.

Services as Software (SaS) – Accelerating AI Deployment

Complementing QAI Studio is Quinnox’s Services as Software (SaS) model, endorsed by a leading analyst firm, HFS Research in their recent report. Services as Software blends the agility of services with the repeatability and scalability of software.

A Services as Software (SaS) operating model reframes enterprise services – IT, operations, and business processes – as modular, productized capabilities. These services are instrumented, automated, governed, and continuously improved using AI, not through manual effort.

In practice, SaS provides the structural foundation that allows AI to move from isolated use cases to repeatable, enterprise-grade capabilities, without inflating cost or risk.

How Quinnox’s Services as Software Operating Model Creates Value

| Lever | What is does | Why it matters | Impact |

|---|---|---|---|

| Platform-led orchestration | Uses agentic AI-driven routing, triage, and self-healing across AMS and integration | Accelerates issue identification, improves throughput, and enables end-to-end vendor visibility | Documented MTTR compression; “watermelon SLA” elimination via shared dashboards |

| Embedded intelligence | Agents learn from logs, behavioral patterns, and system topology | Reduces handoffs and recurring incidents | 30–35% AMS incidents resolved through self healing |

| Value-stream alignment | Organizes delivery pods around domain value flows (e.g., supply chain, omnichannel) | Frees SME capacity for L2/L3 work while stabilizing service quality | 25–40% faster transition using knowledge graphs |

| Outcome-based commercials | Uses interface- or unit-based pricing with flexible capacity models | Delivers cost predictability despite fluctuating demand | Monthly invoicing based on interface volumes rather than headcount |

Together, QAI Studio and the SaS framework provide insurers with a practical, scalable approach to move beyond AI experimentation and embed intelligent automation across their operations.

Ready to operationalize AI at scale? Discover Quinnox’s proven approach for insurers today!

FAQs on AI in Insurance Use Cases

AI detects fraud by identifying anomalies, behavioral patterns, and network connections across thousands of claims simultaneously — catching schemes that rule-based systems routinely miss.

Yes — for simple, low-complexity claims with clear liability and verified coverage, AI can process, approve, and pay without any human involvement, a model known as straight-through processing (STP).

The core barrier is not technology — it is infrastructure: legacy core systems, fragmented data silos, and the lack of a unified data foundation that AI requires to operate accurately at scale.

AI transforms underwriting by automating data extraction, risk scoring, and submission triage — reducing submission-to-quote timelines by 25-40% on average.

Traditional AI performs specific tasks — scoring fraud risk, predicting claims severity, classifying documents — using models trained on labeled historical data. Generative AI (powered by large language models) understands and generates natural language, enabling it to summarize 1,000-page medical files, draft policyholder communications, and answer complex queries conversationally.